Categories

Real EstatePublished June 2, 2025

How Buyers or Sellers Can Buy Down Mortgage Rates to Lower Monthly Payments

When it comes to purchasing a home, one of the most important factors that affects your monthly mortgage payment is the interest rate on your loan. A lower interest rate means lower monthly payments — and over the life of the loan, it can mean tens of thousands of dollars in savings.

What many buyers (and even sellers) don’t realize is that you can actually pay to lower the interest rate on a loan. This is called a mortgage rate buydown, and it can be a smart strategy in the right circumstances.

What Is a Mortgage Rate Buydown?

A rate buydown is when a borrower (or someone on their behalf) pays an upfront fee at closing to get a lower interest rate on their mortgage. This fee is typically paid in the form of “discount points” — each point usually costs 1% of the total loan amount and generally reduces the interest rate by about 0.25%, although the exact benefit varies by lender and market conditions.

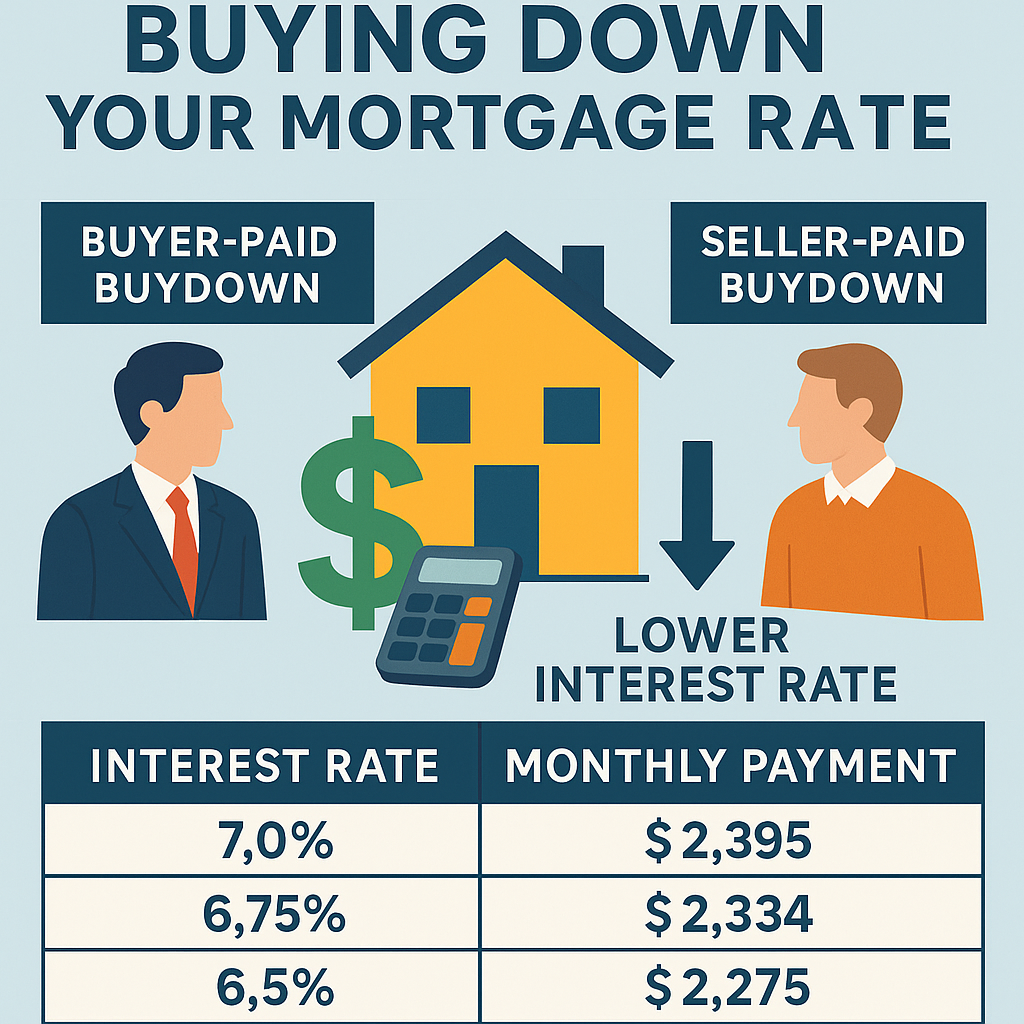

How It Works

Let’s say you’re buying a $400,000 home and taking out a $360,000 loan. The lender offers a 7.0% interest rate, but you want a lower monthly payment. You could pay 1 discount point (1% of the loan amount = $3,600) to bring the rate down to 6.75%. If you pay 2 points ($7,200), maybe you get it down to 6.5%.

Here’s a quick look at how this affects your monthly payment (principal and interest only):

-

7.0% rate: ~$2,395/month

-

6.75% rate: ~$2,334/month

-

6.5% rate: ~$2,275/month

Over the life of a 30-year loan, the savings add up fast.

Who Can Pay for the Buydown?

This is where it gets interesting — either the buyer or the seller can pay for a rate buydown:

1. Buyer-Paid Buydown

Buyers can choose to pay points themselves at closing to lock in a lower rate. This makes the most sense if you:

-

Plan to stay in the home for many years

-

Want a lower monthly payment right away

-

Have extra cash for upfront costs

2. Seller-Paid Buydown (Seller Concessions)

In a slower or buyer-friendly market, sellers may offer to pay for a rate buydown as an incentive to attract buyers. This is especially useful if a buyer is concerned about monthly affordability or high interest rates.

Instead of lowering the sale price, the seller offers a credit (concession) that goes directly toward discount points to reduce the buyer’s rate. The buyer gets a more affordable mortgage, and the seller gets their home sold — it’s a win-win.

Temporary vs. Permanent Buydowns

There are two types of buydowns:

-

Permanent Buydown: The rate is reduced for the life of the loan. This is what we’ve described so far.

-

Temporary Buydown: Often structured as 2-1 or 3-2-1 buydowns. For example, with a 2-1 buydown, your rate is 2% lower in year one, 1% lower in year two, and returns to the full rate in year three. These are often paid for by sellers and are useful for short-term affordability.

Is a Rate Buydown Right for You?

A rate buydown can be a smart move if:

-

You have the cash to pay for points or can negotiate with the seller to cover them

-

You plan to stay in the home long enough to break even on the upfront cost

-

You’re in a high-interest-rate market and want to lock in a lower monthly cost

But remember, it’s not always the best move. If you’re only staying in the home for a few years or rates are expected to drop soon (and you plan to refinance), paying points may not make financial sense.

Final Thoughts

In today’s real estate market, where interest rates may still feel high, understanding how rate buydowns work gives buyers more control over affordability — and gives sellers a valuable tool to make their homes more appealing.

If you’re buying or selling a home, talk to your real estate agent and lender about whether a buydown could work for your situation. A small upfront investment could make a big difference in your long-term finances.

|

or another way